When the Treasury Department announced in early July that employer penalties under the Affordable Care Act (ACA) would be delayed for a year, until 2015, the news came as a relief to long term care providers, regardless of how prepared they were for the transition.

When the Treasury Department announced in early July that employer penalties under the Affordable Care Act (ACA) would be delayed for a year, until 2015, the news came as a relief to long term care providers, regardless of how prepared they were for the transition.

“Delay of the employer mandate meant the delay of both uncertain and actual cost increases,” says Phil Fogg Jr., president and chief executive officer of Marquis Cos. in Milwaukie, Ore.

Marquis had already begun offering an ACA-compliant health plan when the announcement was made. By July, the self-insured organization was preparing its initial communications with employees and was on the brink of offering reduced cost-sharing in the health plan as an incentive for employee participation in wellness initiatives targeting obesity and other costly health problems.

Marquis has about 3,500 employees and operates skilled nursing facilities, assisted living communities, and other long term care services in 26 locations, mostly in Oregon. With a qualifying plan in place, “we are 98 percent of the way there,” Fogg says of Marquis’ readiness for ACA compliance.

He’s less certain, however, about the number and cost of employees who will opt into the health plan, especially as they face the ACA’s individual mandate requiring all adults to obtain insurance for themselves and their children in 2014, or pay a penalty.

Some workers are expected to choose to pay the individual penalty of $95 or 1 percent of household income rather than incur the cost-sharing required by the health plan. Nevertheless, participation in Marquis’ insurance program is expected to spike, adding an estimated $1.5 to $2.5 million a year to benefit costs, Fogg says.

“That’s a big hit for us,” he adds.

Despite the delay in ACA penalties, Marquis’ health coverage will remain intact, along with its commitment to the wellness goals of reducing costs and promoting a healthy workforce. The company has taken a step back, however, from linking wellness participation with financial incentives in the health plan.

Cost Tops List Of Provider Concerns

The ACA requires businesses that are deemed “large employers” to provide health coverage to full-time staff. The coverage must be “affordable” for employees, whose share of premium payments cannot exceed 9.5 percent of their household income. It must also offer “minimum value,” by achieving at least 60 percent actuarial value, meaning the plan can be expected to pay 60 percent of an insured’s health expenses.

Projections of exorbitant cost increases tied to ACA compliance, as well as uncertainty about the magnitude of the increase, and the inability to offset costs by raising prices in a profession dominated by government payers, top the list of long term care providers’ concerns about the ACA.

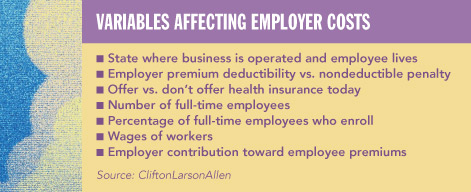

There are no estimates of how much ACA implementation is likely to cost the profession. Financial exposure will vary based on factors unique to each provider and organization, experts say. These include the level of baseline coverage, staff composition and wages, and the number of employees who choose to participate in their employer’s plan.

Providers’ concerns are driven by “two recurring themes,” says Emmett Reed, executive director of the Florida Health Care Association. “It’s going to cost more money, and in some cases a lot more money, to continue operating.”

The second theme is the unknown, he says. Providers don’t know who is going to join the plan and how much more it’s going to cost. As a result, organizations “can’t properly plan their business strategy.”

Some large organizations have estimated as much as a $7 million cost increase, Reed says. “That’s a big number and a huge concern given nursing facilities’ razor-thin margins.” Smaller providers are even more fearful of the impact, he adds. “It’s a frightening time.”

The California Experience

In California, providers are “stepping back and seeing what’s reasonable and what they can afford,” says James Gomez, president and chief executive officer of the California Association of Health Facilities. Unlike Florida, California is integrating the ACA’s optional Medicaid expansion, to 138 percent of the federal poverty level, which will result in the addition of more than 1 million beneficiaries, Gomez says. In addition, the state is running its own Health Insurance Exchange, as opposed to defaulting to the federal government for that function. The Web-based portal could be deluged by 3 million to 4 million registrations for insurance coverage, Gomez says.

“This is a very rapid program that we’re trying to do. It will be difficult everywhere in the nation.”

From providers’ perspective, the effort is draining state and federal resources from quality improvement and the payment of adequate Medicaid rates, he adds.

“We lose money every time we serve a Medicaid participant,” Gomez says. As more people gain eligibility, there is widespread fear across all provider types of further rate erosion.

Under California law, federal and state mandates must be reimbursed, he says. “We’ve let [lawmakers] know this is an issue.”

Craig Robinson, president of Gulf Coast Health Care in Pensa-cola, Fla., says the ACA compounds the uncertainty that long term care providers face from perpetual reimbursement and regulatory changes.

“The [ACA] penalties are being put off, but we need to move forward with health insurance as if it’s going to happen,” he says. “We need to do what we have to by law.” But it’s difficult to do that with “unknown costs” that have to be budgeted, he adds.

“There’s uncertainty in our environment all the time,” stemming from potential payment cuts and regulatory changes, Robinson says.

“The ACA is just like that.”

Gearing Up For Compliance

The year-long reprieve from penalties gives providers additional time to get their arms around the complexities of the ACA, develop health coverage that best fits their organization, and test out their programs before they are exposed to penalties for compliance failures, experts say.

“We’re recommending that employers proceed as if the ACA is going into effect in 2014 and that they use the transition time to work out the kinks, while there are no financial implications from penalties,” says Tiffany Downs, a partner and head of the employee benefits group in the Atlanta law office of Ford Harrison. This gives businesses time to develop Plan B if their initial program isn’t compliant, she adds.

“If you don’t offer coverage at all [during the transition], it takes more time to get up and running.”

Most importantly, the delay should not be mistaken for the demise of the ACA, say legal and health benefits professionals who, like Downs, are advising clients to use the transition time to plan for implementation.

Next year should be treated as “the dry run for employers to see whether the benefits they intend to provide, are going to be compliant in 2015, when ACA penalties kick in,” says Toni Fatone, member services liaison with the American Health Care Association (AHCA), who has worked with insurers and a broker to create the AHCA/National Center for Assisted Living Insurance Solutions Program, which gives members of the organization access to discounted health plans.

“It’s really important that [providers] don’t take their foot off the gas” next year, says Nicole Fallon, a health care consultant at CliftonLarsonAllen (CLA), a national consulting firm based in Minneapolis.

“Employers should use 2013 employee data to simulate how the 2015 requirements will impact their organization, because we believe 2014 data will be used as a measurement period to determine which employees are full-time and which employers are considered ‘large’ and subject to the law,” she says.

It is not clear if the federal government will offer employers the same flexibility in 2015 as it did in 2014, to synchronize the launch of new ACA plans with the start of their existing health plan year or use shorter measurement periods to determine full-time status of employees, says Fallon. If they do not get the same leeway, employers will have to hit the ground running with a compliant plan on Jan. 1, 2015.

“The ACA is not going to go away,” says Nancy Taylor, an attorney with the Miami-based law firm Greenberg Traurig and co-chair of the firm’s health and FDA business practice. “It’s wishful thinking to believe it could be delayed forever.”

Providers wrestling with ACA compliance must also wrestle with math. The law is stacked with formulas and measurements that determine whether a provider is subject to penalties for failing to offer health coverage, whether workers are counted as full-time and must therefore be offered coverage, whether health benefits meet value and affordability tests, and whether a provider and its workforce would be better served by compliance or penalty payment.

These often dizzying calculations are staples of ACA webinars, workshops, and presentations being conducted nationwide for long term care and other employers, by legal and benefits experts who are steeped in details of the law.

ACA calculus begins with staffing. Only businesses with 50 or more full-time employees and “equivalents” are deemed to be large employers, subject to the ACA’s health coverage requirements and at risk of penalties for failing to comply.

Counting staff, however, is not as simple as it sounds. The ACA defines full time as 30 hours per week, measured as 130 hours of service in a month, says Taylor, who also serves as legal counsel to AHCA and has conducted several ACA webinars and presentations for the organization and its state affiliates.

For the purpose of determining whether a business is a large employer, however, the count includes the total hours worked by all part-time staff in a month, up to a maximum of 120 hours per employee, divided by 120, Taylor explained in a July webinar for AHCA. The sum of that equation is the number of “full-time equivalents,” which must be added to the number of actual full-time workers. If the final tally is 50 or more, the business meets the definition.

Look-Back Period

For staff whose full- or part-time status is unclear due to their variable or seasonal schedule, the ACA creates a “look-back” period.

This measurement tool allows employers to track an employee’s hours over a three- to 12-month period to determine whether they average 30 hours per week/130 hours per month, says Downs. If so, the person is deemed full time and must be offered health coverage during a “stability period” of six months, or the duration of the look-back, whichever is greater, Downs says.

Employers may designate an administrative period up to 90 days between the look-back and stability periods, in which they “crunch numbers and offer enrollment,” Downs says. At the end of 90 days, the stability period must start immediately, and employers must provide health coverage to those workers deemed full-time, even if their hours no longer rise to the level of full-time status, Downs says.

A look-back period can only be used when “it’s not clear that an employee works 30 hours a week,” Downs says. “It cannot be used to delay coverage. There has to be a determination that hours really are variable.”

The ACA And Quality Care

As employers develop strategies for managing ACA costs and meeting compliance challenges, one of the available options is to create more part-time positions, reducing the number of staff to whom insurance coverage must be offered.

While the approach might be useful in retail or other settings, long term care providers are not embracing part-time employment as a solution.

At Mission Health Services in Ogden, Utah, the philosophy of care is rooted in the belief that “the resident has to be well-known,” says Gary Kelso, president and chief executive officer. “That means we have to have consistent staffing.”

By having “the same individuals caring for people every day, even if there is a slight change in condition, the employee will see it,” Kelso says.

The need for consistency and familiarity means that reducing work hours to create more part-time staff who don’t have to be offered health coverage under the ACA is not an option for Mission Health, a nonprofit with four facilities and 375 employees. The organization, which is partially self-insured, put an employee insurance plan in place five years ago. It covers 100 percent of employees’ premium cost, has a small copay after the deductible is met, and needs no modifications to comply with the ACA.

Since the plan was implemented, Mission Health’s workers’ compensation costs have dropped dramatically, and staff turnover has plummeted from 60 to 70 percent, which is typical in the long term care sector, to under 10 percent for the past three years, Kelso says. All facilities have four or five stars from the Centers for Medicare & Medicaid Services, and two have had deficiency-free surveys for the past 18 months.

Other factors have likely contributed to these trends, including the fact that all Mission Health facilities are Eden-registered, Kelso says. While he believes the ACA is “bad policy” that will lead to “losses in business and losses in the economy,” he’s not expecting to reduce employees to part time.

“I don’t think that’s a valuable or good policy,” he says.

Kelso says he’s not stressed about the ACA, as there’s nothing the organization needs to change to be compliant. The acquisition of 12 facilities, with 475 employees, is on the horizon, however, and the move may add as much $1 million a year to the health benefits rate structure.

“That’s significant,” Kelso says. “We may have to ask employees to pay a small amount” for their premiums, though it would probably not be as much as the ACA’s benchmark for affordability, which is 9.5 percent of household income.

“That’s still too high in my perspective when you have lower-paid employees,” he says.

Creating A Workable Plan

At Opis Management Resources in Tampa, Fla., the company is working closely with a health insurance broker to understand the ACA, the changes that it would have to make to come into compliance, options for redesigning the current benefit program, and the associated costs.

“We’ve always provided coverage and have a generous plan,” which is “extremely affordable” and has a good participation rate, says Jennifer Ziolkowski, senior vice president of finance. Adding staff who work 30 hours a week, as opposed to the current 32-hour threshold for full-time status, will be the biggest cost, she says.

Opis manages 10 Florida skilled nursing facilities and one assisted living community. With about 2,300 employees, the company recognizes the need to remain competitive, and that means keeping up with the benefits that other providers and other types of businesses are offering. Opis plans to come into ACA compliance, and doing so will require closer management of staff hours, Ziolkowski says.

In looking closely at monthly reports on “flex staff,” who are supposed to be part-time, for example, Opis found that some of those employees were in fact working 40 hours a week.

“We were calling them as needed, but we needed them all the time,” Ziolkowski says. “Our mindset isn’t on having more flex-time workers, but on having permanent staff,” she says.

As the organization focuses more closely on hours, it will have to be vigilant about defining full-time, part-time, and flex staff, she says.

“We need to make sure that if we have flex staff working more than what we consider flex time, we address that by approaching staff to become full time, or by spreading the hours over more people,” she says.

Next to managing the cost of ACA compliance, the greatest challenge faced by long term care providers will be the time and effort it takes to track employee hours and other data required by the ACA, says CLA’s Fallon.

“A large organization with a couple of hundred employees and on-call staff now has to closely track all those hours.”

Pay Or Play: That Is The Question

Among the most critical ACA calculations employers have to make is the decision to offer health coverage or pay a penalty.

Many factors go into this consideration, says Fallon, including staff composition and wage levels, premiums charged by the Health Insurance Exchange, and the cost of providers’ options.

Under the ACA, providers that don’t offer any health coverage to full-time workers are subject to a $2,000 penalty for every full-time worker in their employ, excluding the first 30.

Employers that offer insurance that fails to meet the ACA’s affordability or minimum value test are subject to a higher penalty of $3,000, but it applies only to full-time employees who receive subsidies through the Health Insurance Exchange, as opposed to the entire full-time staff.

To be affordable, employees’ share of the premium cannot exceed 9.5 percent of their modified adjusted gross household incomes. Alternatively, IRS regulations provide employers three affordability safe harbors: 9.5 percent of the employee’s W-2 wages, 9.5 percent of the federal poverty level, or 9.5 percent of their monthly wages based on 130 hours of service and their hourly rate of pay.

Employers incur no penalties unless a full-time employee applies to the Exchange for coverage and is deemed eligible for subsidies.

“A penalty is tied to a full-time person,” Fallon says. “You only trip the trigger on a penalty if a person goes to the Exchange and purchases insurance with sudsidies.”

A Health Insurance Exchange is an ACA-created entity designed to function as a Web-based marketplace for individual and small-group health plans.

The Exchange is also a portal where individuals with incomes up to 400 percent of the federal poverty level ($45,960 for an individual and $94,200 for a family of four) may apply for sliding-scale premium tax credits and cost-sharing subsidies.

Employees who earn more than 400 percent of poverty are not eligible for subsidies and therefore will not trigger employer penalties, even if they purchase insurance via one of the Exchanges, says Fallon.

States Choose Exchange Type

Exchanges can be unilaterally created and controlled by the state, or run solely by the federal government, or operated through a partnership between state and federal agencies.

According to the Kaiser Family Foundation, as of late May 2013, 17 states had announced plans to create their own exchanges, retaining control over all activities, including selection of health plans. Twenty-six states had defaulted to a federal exchange, while another seven were planning a partnership exchange.

Insurance plans sold through the Exchange must meet one of four “actuarial value” tiers, designated by the ACA as bronze, silver, gold, and platinum, the Kaiser Family Foundation reported in a 2011 analysis of ACA actuarial values.

An actuarial value is the percentage of health care expenses a health plan is expected to pay, based on a standard population, Kaiser said. The ACA requires minimum-level bronze plans to meet a 60 percent actuarial value, meaning consumers can expect to pay 40 percent of their health expenses out-of-pocket, through deductibles, copays, and coinsurance.

The ACA requires at least a 60 percent actuarial value, which is referred to as the “minimum value,” for any health plan purchased by individuals through the Exchange, or offered by employers to full-time staff.

The highest tier platinum plans, for people with incomes from 100 percent to 150 percent of poverty, have a 94 percent actuarial value, according to Kaiser.

Insurance subsidies will be administered through the Exchange via federal payments to insurers for reducing premium costs and, in some cases, cost-sharing for low-income purchasers, CLA says. Households with incomes up to 200 percent of poverty, for example, are eligible for a two-thirds cost-sharing reduction, while those between 200 percent and 250 per-cent may receive a 50 percent subsidy to reduce out-of-pocket costs, according to materials prepared by CLA.

The premiums, benefits, and provider networks available through Exchanges will vary from state to state, sometimes dramatically, says Fallon. Employers should be aware of what their Exchange is offering to understand how it compares with what they can afford to offer employees, Fallon says. Low-income workers might find more affordable coverage through the Exchange with or, in some cases, even without subsidies, though they would only be eligible for financial assistance, if their employer did not offer coverage, or failed to offer an affordable, minimum-value plan, she adds.

To help providers determine the most cost-effective option, AHCA offers its membership a free comparison of their penalty and coverage costs. The service is part of a larger AHCA/NCAL Insurance Solutions Program, which gives members access to national carriers that have agreed to offer members discounted coverage for their workforces, including options for providers that want to self-insure, says Fatone.

AHCA has also partnered with Benefit Focus, a human resources software firm that can manage much of the employee data collection and reports required for the ACA, Fatone says. While the cloud-based service isn’t free, it creates tremendous efficiencies for employers.

Lynn Wagner is a freelance writer based in Shepherdstown, W.Va.